As employers evaluate funded End-of-Service Benefits (EOSB) arrangements, one practical question often arises: how can businesses absorb a recurring EOSB funding obligation without creating operational strain?

It is an important consideration, particularly for organisations that have historically treated EOSB as a balance sheet provision rather than a recurring cashflow item.

Let's remember: regardless of short-term business conditions, EOSB liabilities continue to accumulate. So regularly funding and ringfencing EOSB should be a finance discipline irrespective of whether an employer enrols in a funded scheme.

Based on discussions with employers and consultants, there are three practical steps Finance teams can consider.

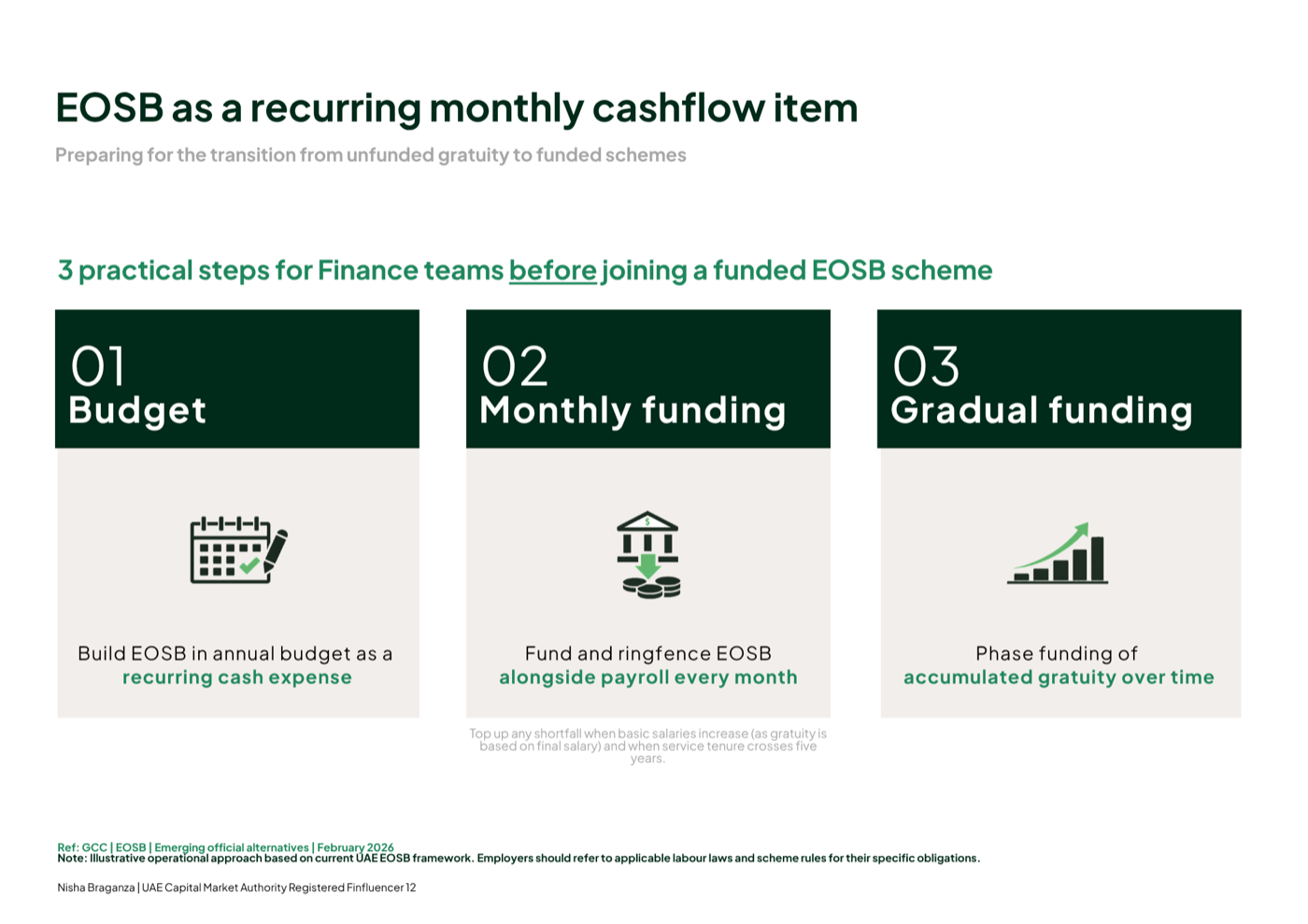

1. Build EOSB into annual budgets

Rather than viewing EOSB as a growing balance sheet provision, employers can budget for it as a recurring monthly cash expense. This helps make EOSB funding part of normal business planning and reduces the risk of unexpected cashflow pressures in the future.

2. Set aside EOSB accruals each month

Employers may wish to set aside EOSB accruals alongside payroll on a monthly basis. As a reference point, this broadly equates to:

- Approximately 5.83% of basic salary for employees with less than five years of service.

- Approximately 8.33% of basic salary for employees with more than five years of service.

Employers should also remember that gratuity is calculated using final basic salary. As salaries increase and employees cross key service milestones, additional funding may be required to address any shortfall.

3. Put a plan in place to gradually fund accumulated liabilities

Many employers have existing gratuity obligations that have built up over time.

Rather than waiting until employees leave or until a future transition to a funded scheme, organisations may find it beneficial to gradually fund accumulated liabilities over a defined period. This can help smooth cashflow requirements and reduce the risk of large one-off outflows.

Looking ahead

Employers that treat EOSB as a recurring funding obligation rather than a future liability are generally better positioned to manage employee exits and prepare for any future transition to a funded EOSB scheme.

While every organisation will have different circumstances, proactive funding can help reduce uncertainty and improve long-term financial planning.

Nisha Braganza

Founder and CEO, Vestora · UAE CMA Registered Finfluencer No. 12

Independent commentary on EOSB markets and regulation across the UAE and GCC.